Lithium-Ion Battery Recycling Market Report 2025: In-Depth Analysis of Growth Drivers, Technology Innovations, and Global Opportunities. Explore Market Size, Key Players, and Forecasts Through 2030.

- Executive Summary & Market Overview

- Key Market Drivers and Restraints

- Technology Trends in Lithium-Ion Battery Recycling

- Competitive Landscape and Leading Players

- Market Size and Growth Forecasts (2025–2030)

- Regional Analysis: North America, Europe, Asia-Pacific, and Rest of World

- Challenges and Opportunities in the Recycling Value Chain

- Regulatory Environment and Policy Impact

- Future Outlook: Emerging Trends and Strategic Recommendations

- Sources & References

Executive Summary & Market Overview

The global lithium-ion battery recycling market is poised for significant growth in 2025, driven by the rapid expansion of electric vehicles (EVs), consumer electronics, and energy storage systems. Lithium-ion batteries, essential for these applications, have a finite lifespan, leading to a surge in end-of-life batteries requiring sustainable disposal and resource recovery solutions. Recycling not only mitigates environmental hazards associated with improper disposal but also addresses the supply chain risks and price volatility of critical raw materials such as lithium, cobalt, and nickel.

According to Allied Market Research, the global lithium-ion battery recycling market was valued at approximately $1.7 billion in 2022 and is projected to reach over $6.5 billion by 2032, with a compound annual growth rate (CAGR) exceeding 14% during the forecast period. The year 2025 is expected to mark a pivotal point, as regulatory frameworks in regions such as the European Union and China become more stringent, mandating higher recycling rates and extended producer responsibility for battery manufacturers.

Key market drivers in 2025 include:

- Accelerated adoption of EVs, with global sales expected to surpass 17 million units, resulting in a growing volume of spent batteries entering the recycling stream (International Energy Agency).

- Technological advancements in recycling processes, such as hydrometallurgical and direct recycling methods, which improve material recovery rates and economic viability (IDTechEx).

- Strategic investments and partnerships among automakers, battery manufacturers, and recycling firms to secure critical material supply and comply with evolving regulations (BASF).

Regionally, Asia-Pacific dominates the market, led by China’s aggressive policy mandates and industrial capacity, while Europe and North America are rapidly scaling up their recycling infrastructure in response to local battery production and end-of-life management needs. The competitive landscape is characterized by the emergence of specialized recyclers, such as Umicore and Li-Cycle, alongside traditional waste management and mining companies diversifying into battery recycling.

In summary, 2025 will be a transformative year for lithium-ion battery recycling, as the industry responds to mounting environmental, regulatory, and supply chain pressures, positioning itself as a critical enabler of the global energy transition.

Key Market Drivers and Restraints

The lithium-ion battery recycling market in 2025 is shaped by a dynamic interplay of drivers and restraints, reflecting both the rapid expansion of battery-dependent industries and the challenges inherent in recycling technologies and infrastructure.

Key Market Drivers

- Surging Electric Vehicle (EV) Adoption: The global shift toward electric mobility is a primary catalyst, with EV sales projected to reach 17 million units in 2025, up from 10.5 million in 2022. This surge is generating a significant volume of end-of-life batteries, intensifying the need for efficient recycling solutions (International Energy Agency).

- Regulatory Mandates and Circular Economy Initiatives: Governments in the EU, China, and North America are implementing stringent regulations to ensure responsible battery disposal and promote recycling. The European Union’s Battery Regulation, effective from 2025, mandates minimum recycled content in new batteries and sets ambitious collection and recycling targets (European Commission).

- Resource Security and Raw Material Prices: The volatility and rising costs of critical battery materials—such as lithium, cobalt, and nickel—are prompting manufacturers to secure secondary sources through recycling. This not only reduces supply chain risks but also supports sustainability goals (Benchmark Mineral Intelligence).

- Technological Advancements: Innovations in hydrometallurgical and direct recycling processes are improving recovery rates and reducing costs, making recycling more economically viable and environmentally friendly (IDTechEx).

Key Market Restraints

- Technical Complexity and Safety Risks: The diversity of battery chemistries and designs complicates disassembly and material recovery. Safety concerns, such as fire hazards during transport and processing, further hinder large-scale operations (Organisation for Economic Co-operation and Development).

- Economic Viability: Fluctuating prices for recovered materials and high initial investment costs for recycling facilities can undermine profitability, especially in regions with limited policy support (McKinsey & Company).

- Collection and Logistics Challenges: Inefficient collection systems, lack of consumer awareness, and logistical hurdles in transporting spent batteries from dispersed sources to recycling centers remain significant barriers (Wood Mackenzie).

Technology Trends in Lithium-Ion Battery Recycling

Lithium-ion battery recycling is undergoing rapid technological transformation as the global demand for electric vehicles (EVs), consumer electronics, and energy storage systems accelerates. In 2025, several key technology trends are shaping the industry, driven by the need to recover valuable materials, reduce environmental impact, and address supply chain vulnerabilities.

One of the most significant trends is the shift from traditional pyrometallurgical and hydrometallurgical processes to advanced direct recycling methods. Direct recycling, also known as cathode-to-cathode recycling, aims to preserve the structure of cathode materials, enabling their direct reuse in new batteries. This approach reduces energy consumption and chemical waste compared to conventional methods. Companies such as Redwood Materials and Li-Cycle Holdings Corp. are investing heavily in scaling up these processes, with pilot plants demonstrating promising recovery rates and material purity.

Automation and artificial intelligence (AI) are increasingly integrated into battery sorting and disassembly. Automated systems use robotics and machine vision to identify battery chemistries, assess state-of-health, and safely dismantle battery packs. This not only improves worker safety but also enhances throughput and material recovery efficiency. Umicore and Ecobat are among the industry leaders deploying such technologies in their recycling facilities.

Another notable trend is the development of closed-loop supply chains, where recycled materials are directly reintegrated into new battery manufacturing. Automakers like Tesla, Inc. and Volkswagen AG are partnering with recyclers to secure sustainable sources of lithium, cobalt, and nickel, reducing reliance on virgin mining and improving the overall sustainability profile of EVs.

- Solvent-based extraction: Innovations in green solvents and selective leaching agents are improving the efficiency and environmental footprint of hydrometallurgical recycling.

- Decentralized recycling: Modular, mobile recycling units are being deployed to process batteries closer to the point of collection, reducing transportation costs and emissions.

- Data-driven traceability: Blockchain and digital tracking systems are being implemented to ensure transparency and regulatory compliance throughout the recycling value chain.

These technology trends are expected to accelerate the growth and efficiency of the lithium-ion battery recycling market in 2025, supporting the transition to a circular battery economy and helping to meet the surging demand for critical battery materials worldwide (International Energy Agency).

Competitive Landscape and Leading Players

The competitive landscape of the lithium-ion battery recycling market in 2025 is characterized by rapid expansion, strategic partnerships, and significant investments from both established industry leaders and innovative startups. As the global demand for electric vehicles (EVs) and energy storage systems accelerates, the need for sustainable end-of-life battery management has intensified, driving competition among recyclers to secure supply contracts, develop advanced technologies, and scale operations.

Key players in the market include Umicore, Retriev Technologies, Li-Cycle Holdings Corp., Ecobat, and GEM Co., Ltd.. These companies have established robust collection networks and proprietary recycling processes, such as hydrometallurgical and pyrometallurgical methods, to recover valuable metals like lithium, cobalt, and nickel from spent batteries. For instance, Umicore operates one of the largest closed-loop battery recycling facilities in Europe, while Li-Cycle Holdings Corp. has expanded its spoke-and-hub model across North America, aiming to process up to 35,000 tonnes of lithium-ion batteries annually by 2025.

Asian companies, particularly in China, are also dominant players. GEM Co., Ltd. and Brilliant Technology have leveraged government support and proximity to battery manufacturing hubs to scale their recycling capacities. According to Benchmark Mineral Intelligence, China accounted for over 60% of global lithium-ion battery recycling capacity in 2024, a trend expected to continue into 2025.

Startups and technology disruptors are intensifying competition by introducing novel recycling techniques. Companies like Redwood Materials and Ascend Elements are attracting significant venture capital and forming partnerships with automakers such as Ford Motor Company and Tesla, Inc. to secure feedstock and offtake agreements. These collaborations are crucial for ensuring a steady supply of end-of-life batteries and for meeting increasingly stringent regulatory requirements on battery recycling and material circularity.

Overall, the 2025 market is marked by consolidation, cross-sector alliances, and a race to achieve technological breakthroughs that improve recovery rates and reduce costs, positioning leading players to capture a growing share of the global lithium-ion battery recycling value chain.

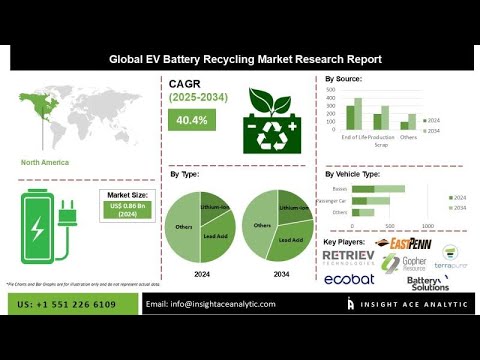

Market Size and Growth Forecasts (2025–2030)

The global lithium-ion battery recycling market is poised for significant expansion in 2025, driven by surging demand for electric vehicles (EVs), energy storage systems, and portable electronics. According to MarketsandMarkets, the market size is projected to reach approximately USD 9.2 billion in 2025, up from an estimated USD 6.5 billion in 2023. This robust growth is underpinned by increasing end-of-life battery volumes, regulatory mandates for sustainable waste management, and the rising value of recovered materials such as lithium, cobalt, and nickel.

From 2025 to 2030, the lithium-ion battery recycling market is expected to register a compound annual growth rate (CAGR) of 20–23%, with forecasts suggesting the market could surpass USD 22 billion by 2030. This acceleration is attributed to several converging factors:

- EV Adoption: The International Energy Agency (IEA) projects global EV stock to exceed 145 million by 2030, resulting in a substantial increase in spent batteries requiring recycling.

- Regulatory Pressure: The European Union’s Battery Regulation and similar policies in China and the United States are mandating higher recycling rates and extended producer responsibility, directly stimulating market growth (European Commission).

- Technological Advancements: Innovations in hydrometallurgical and direct recycling processes are improving recovery rates and economic viability, making recycling more attractive for industry stakeholders (IDTechEx).

Regionally, Asia-Pacific is expected to maintain its dominance in 2025, accounting for over 40% of global market share, led by China, Japan, and South Korea. North America and Europe are anticipated to experience the fastest growth rates, propelled by aggressive EV targets and substantial investments in recycling infrastructure (Fortune Business Insights).

In summary, 2025 marks a pivotal year for the lithium-ion battery recycling market, setting the stage for rapid expansion through 2030. The interplay of regulatory action, technological progress, and the EV revolution will continue to drive market size and growth, positioning recycling as a critical component of the global battery value chain.

Regional Analysis: North America, Europe, Asia-Pacific, and Rest of World

The global lithium-ion battery recycling market in 2025 is characterized by significant regional disparities in terms of capacity, regulatory frameworks, and technological adoption. The four key regions—North America, Europe, Asia-Pacific, and Rest of World—each present unique dynamics that shape the industry’s trajectory.

- North America: The North American market, led by the United States and Canada, is experiencing rapid growth due to increasing electric vehicle (EV) adoption and government incentives for battery recycling. The U.S. Department of Energy’s Battery Recycling Prize and investments in domestic recycling infrastructure are driving innovation and capacity expansion. Major players such as Redwood Materials and Li-Cycle are scaling up operations, with new facilities coming online in 2025. The region’s regulatory environment is evolving, with several states considering extended producer responsibility (EPR) laws for batteries, further supporting market growth.

- Europe: Europe remains at the forefront of lithium-ion battery recycling, propelled by stringent EU regulations such as the Battery Directive and the upcoming Battery Regulation, which mandates high recycling efficiency and material recovery rates. Countries like Germany, France, and Belgium are home to advanced recycling facilities operated by companies like Umicore and Northvolt. The European Commission’s push for a circular battery value chain and the localization of battery manufacturing are expected to further boost recycling volumes in 2025, with the region targeting a closed-loop system for critical materials.

- Asia-Pacific: Asia-Pacific, particularly China, Japan, and South Korea, dominates global lithium-ion battery recycling capacity. China’s government mandates for battery collection and recycling, coupled with the world’s largest EV market, have led to the emergence of major recyclers such as GEM Co., Ltd. and Brilian. Japan and South Korea are investing in advanced hydrometallurgical and direct recycling technologies. The region’s growth is underpinned by strong supply chain integration and government support, with 2025 expected to see further capacity expansions and technology upgrades.

- Rest of World: In regions outside the major markets, lithium-ion battery recycling remains nascent but is gaining traction. Countries in Latin America, the Middle East, and Africa are beginning to establish pilot projects and regulatory frameworks, often in partnership with international organizations and technology providers. Growth in these regions is expected to accelerate post-2025 as EV adoption rises and global supply chains seek new sources of recycled materials.

Challenges and Opportunities in the Recycling Value Chain

The recycling value chain for lithium-ion batteries (LIBs) in 2025 faces a complex landscape of challenges and opportunities, shaped by surging demand for electric vehicles (EVs), evolving regulatory frameworks, and rapid technological advancements. As global EV adoption accelerates, the volume of end-of-life LIBs is projected to increase significantly, intensifying the need for efficient and sustainable recycling solutions.

Challenges:

- Collection and Logistics: The fragmented collection infrastructure for spent LIBs remains a major bottleneck. Many batteries are dispersed across consumer electronics, industrial applications, and vehicles, complicating aggregation and transportation. Safety concerns, such as fire risks during handling and transit, further exacerbate logistical hurdles (International Energy Agency).

- Technological Limitations: Current recycling methods—primarily pyrometallurgical and hydrometallurgical processes—face limitations in recovering high-purity materials, especially lithium. Direct recycling, which preserves cathode structure, is promising but not yet widely commercialized (IDTechEx).

- Economic Viability: Fluctuating prices for recovered materials, such as cobalt and nickel, impact the profitability of recycling operations. Additionally, the declining cobalt content in next-generation batteries may reduce the economic incentive for recyclers (Benchmark Mineral Intelligence).

- Regulatory Uncertainty: While the European Union’s Battery Regulation is setting ambitious recycling targets, global regulatory alignment is lacking. Inconsistent standards and extended producer responsibility (EPR) schemes create compliance challenges for multinational companies (European Commission).

Opportunities:

- Resource Security: Recycling offers a strategic pathway to secure critical raw materials, such as lithium, nickel, and cobalt, reducing dependence on volatile global supply chains and supporting domestic battery manufacturing (U.S. Geological Survey).

- Technological Innovation: Advances in direct recycling, automation, and AI-driven sorting are poised to improve material recovery rates and lower costs. Companies investing in R&D and scaling innovative processes stand to gain a competitive edge (BloombergNEF).

- Policy Support: Strengthening EPR policies, harmonizing international standards, and incentivizing recycling infrastructure investment can accelerate market growth and create new business models, such as battery-as-a-service and closed-loop supply chains (International Energy Agency).

In summary, while the LIB recycling value chain in 2025 is challenged by collection, technology, economics, and regulation, it is also ripe with opportunities for innovation, resource security, and policy-driven growth.

Regulatory Environment and Policy Impact

The regulatory environment for lithium-ion battery recycling is rapidly evolving in response to the surging demand for electric vehicles (EVs), energy storage systems, and portable electronics. In 2025, governments worldwide are intensifying efforts to address the environmental and supply chain challenges posed by end-of-life lithium-ion batteries. Regulatory frameworks are increasingly focused on promoting circular economy principles, ensuring safe handling, and securing critical raw materials such as lithium, cobalt, and nickel.

In the European Union, the revised Batteries Regulation, which came into force in 2023, is a key driver shaping the 2025 landscape. The regulation mandates higher collection targets, minimum recycled content requirements, and strict due diligence obligations for battery producers. By 2025, battery manufacturers must ensure that new batteries contain a minimum percentage of recycled materials—16% for cobalt, 6% for lithium, and 6% for nickel—creating strong incentives for investment in recycling infrastructure and technology (European Commission).

In the United States, regulatory oversight is more fragmented, with state-level initiatives complementing federal guidelines. The Bipartisan Infrastructure Law (2021) allocated significant funding for battery recycling research and pilot projects, and the Department of Energy continues to support the development of a domestic battery recycling supply chain. In 2025, California’s Battery Recycling Act and similar state policies are expected to set precedents for extended producer responsibility (EPR) and mandatory collection schemes (U.S. Department of Energy).

China, the world’s largest EV market, has implemented stringent regulations requiring automakers and battery manufacturers to establish traceable recycling channels and meet specific recovery rates for key metals. The 2025 regulatory focus is on scaling up closed-loop recycling systems and enforcing compliance through digital tracking platforms (Ministry of Industry and Information Technology of the People’s Republic of China).

- Regulatory harmonization remains a challenge, with varying standards and reporting requirements across regions.

- Policy uncertainty and evolving compliance costs are influencing investment decisions and technology adoption in the recycling sector.

- Stricter regulations are expected to accelerate innovation in recycling processes, such as hydrometallurgical and direct recycling methods.

Overall, the 2025 regulatory environment is a catalyst for market growth, technological advancement, and supply chain resilience in lithium-ion battery recycling, but it also introduces complexity and compliance risks for industry stakeholders.

Future Outlook: Emerging Trends and Strategic Recommendations

The future outlook for lithium-ion battery recycling in 2025 is shaped by accelerating electric vehicle (EV) adoption, tightening regulatory frameworks, and rapid technological advancements. As global EV sales are projected to surpass 17 million units in 2025, the volume of end-of-life batteries entering the recycling stream will increase substantially, intensifying the need for efficient and scalable recycling solutions (International Energy Agency).

Emerging Trends

- Direct Recycling and Advanced Recovery Technologies: Innovations such as direct cathode-to-cathode recycling and hydrometallurgical processes are gaining traction, offering higher material recovery rates and lower environmental impact compared to traditional pyrometallurgical methods. Companies like Redwood Materials and Li-Cycle Holdings Corp. are scaling up these technologies to commercial levels.

- Integration with Battery Manufacturing: Closed-loop systems, where recycled materials are directly reintegrated into new battery production, are becoming a strategic priority for automakers and battery manufacturers. Tesla and CATL have announced initiatives to source a significant portion of their raw materials from recycled batteries by 2025.

- Policy and Regulatory Drivers: The European Union’s Battery Regulation, set to take effect in 2025, mandates minimum recycled content in new batteries and strict collection targets, setting a global benchmark for other regions (European Commission).

- Global Expansion and Localization: North America, Europe, and Asia are witnessing a surge in new recycling facilities, with investments from both public and private sectors. Localization of recycling capacity is seen as critical for supply chain resilience and reducing transportation emissions.

Strategic Recommendations

- Invest in Next-Generation Technologies: Stakeholders should prioritize R&D in direct recycling and digital tracking of battery materials to maximize recovery rates and traceability.

- Forge Strategic Partnerships: Collaboration between automakers, recyclers, and raw material suppliers will be essential to build closed-loop supply chains and meet regulatory requirements.

- Prepare for Regulatory Compliance: Companies must proactively align with upcoming regulations, particularly in the EU and China, to avoid market access barriers and capitalize on incentives.

- Scale Infrastructure: Expanding collection networks and recycling capacity will be vital to handle the anticipated surge in end-of-life batteries and to secure critical materials for future battery production.

In summary, 2025 will mark a pivotal year for lithium-ion battery recycling, with technology, policy, and industry collaboration converging to drive a more circular and sustainable battery ecosystem.

Sources & References

- Allied Market Research

- International Energy Agency

- BASF

- Umicore

- Li-Cycle

- European Commission

- Benchmark Mineral Intelligence

- McKinsey & Company

- Wood Mackenzie

- Redwood Materials

- Ecobat

- Volkswagen AG

- Retriev Technologies

- GEM Co., Ltd.

- MarketsandMarkets

- Fortune Business Insights

- Northvolt

- European Commission

- BloombergNEF

- CATL